You just finished your pitch, and you think you nailed it. You’re feeling good.

As you log off zoom or leave the conference room you’re probably thinking: What are the investors thinking right now?

Let us pull the curtains back a bit. The investors you just pitched look at each other for a moment. In that moment there’s an ineffable energy. It goes one of two ways:

Option 1: 100% energy. We want to run through a wall. Start due diligence right away. Call our partners and tell them about you.

Or Option 2: It’s quiet, and people shrug and look at each other. There’s just a feeling that this is not the one.

We live for option 1, we love that energy. That’s why we’re excited to go to work and listen to so many pitches. But sadly, it’s rare. If you end up in option 2, it’s very hard to move into option 1 territory.

That initial feeling matters more than anyone would like to admit.

To make matters worse, if you are in the “option 2” category, most VCs won’t even tell you the real reason why. The worst of us will be assholes, and drag you along while they are waiting to see if some other “top VC” firm makes up their mind.

We’ve already written about what we look for when we invest in companies. The hardest feedback to give isn’t about the defensible magical technology, or the market, it’s about the people.

Sometimes, when a VC doesn’t invest, it’s about you. Or, more accurately, their perception of you.

This is even true in bio where great science and IP is a big part of the story. It is extremely true in software, where pivots are guaranteed.

Investing at seed is investing in people. Your investors have to feel that you are the person who can go the distance from seed to a massive exit. This is the hardest feedback to give, because it doesn’t feel actionable.

I’m writing this because I believe there’s something you can do if you see the whole picture. Even with great IP and a market big enough for venture returns, it’s a missed opportunity if you don’t recognize that many VCs look for specific “intangibles” during pitches.

So, from my perspective as a founder who wrote 148 pitch decks, and a VC who sees thousands of deals every year: this is how to avoid the “option 2” zone.

The Best Case Scenario

When investors are energized about a founder, they often use one word to describe that person:

This is the magic word.

Of course, this is absolutely useless to you. How are you supposed to know what one particular VC finds compelling?

When most VCs find someone compelling, they mean: I have to invest in this person – it’s a hard feeling to describe, but we know it when we see and feel it.

The closest thing I can think of to describe this is the concept of “intangibles” in football. When assessing a potential NFL quarterback, scouts will grade candidates on accuracy, footwork, strength, etc…but also on an aspect of their game that’s impossible to quantify directly. Intangibles are the gut feeling a scout gets that this person is a winner. We all know that feeling… it’s how we feel when Tom Brady, or Patrick Mahomes is down in the fourth quarter with a few minutes to go – we all know they will drive down the field and win.

Once you become successful, everyone will say you had it in you all along. The key is convincing someone you have that kind of potential when you’re just starting out.

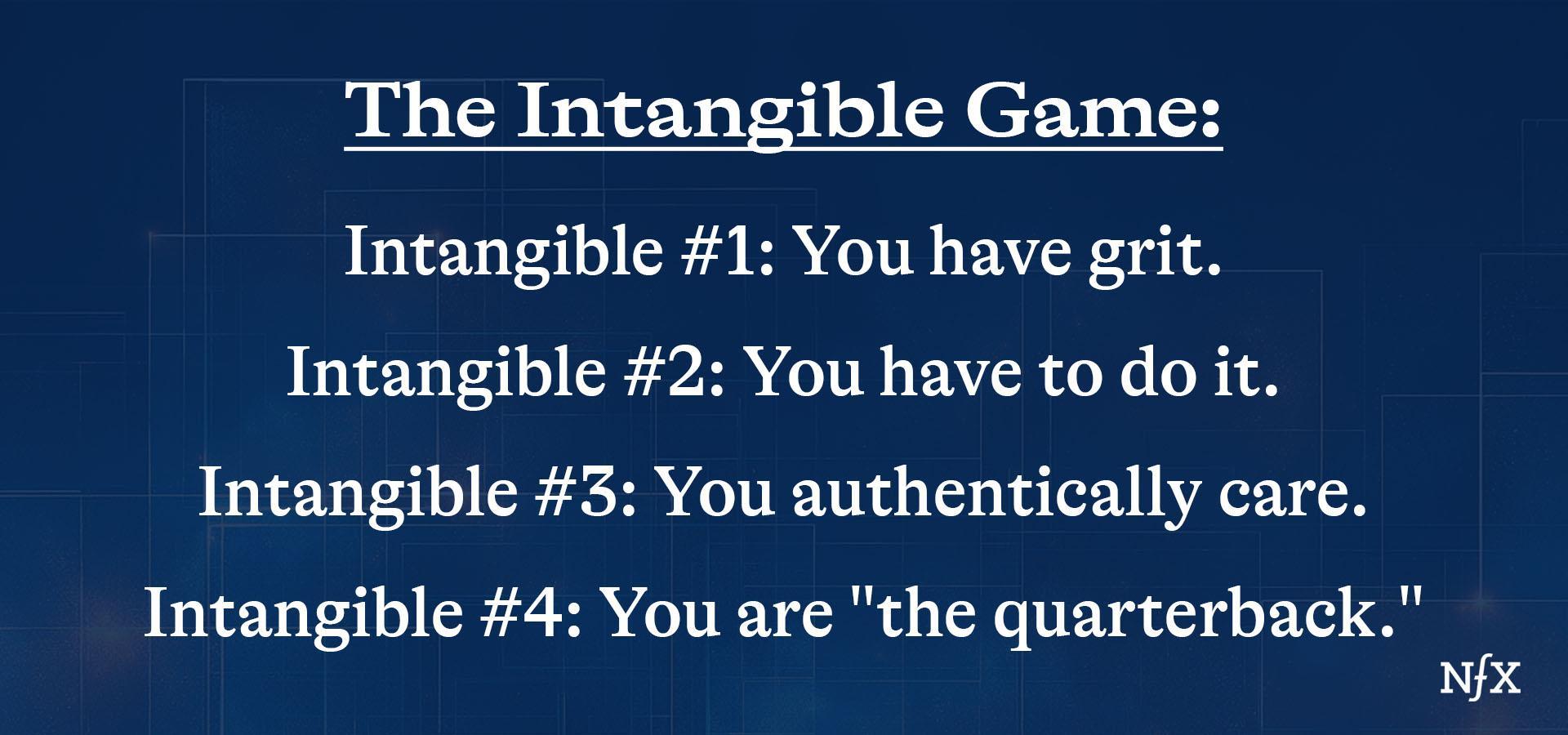

So while no one can provide a perfectly accurate map of founder “intangibles,” these are the elements that get somewhat close.

Intangible #1: You Have Grit

Starting a company is a worthwhile way to spend your life. But most of the time, it’s hard.

My short definition of a founder’s job: suffer stoically.

Your health will suffer.

Your relationships will suffer.

You will suffer from endless FOMO and imposter syndrome – why is everyone raising, hiring, growing, when I’m not?

You will feel like you don’t know what you’re doing half the time.

You will struggle in ways you can predict,

And in ways you can’t predict.

When I was a CEO, during the dark times I personally felt this as the “clenching feeling of death.” deep in my guts.

Read that all again. Think about your life now. Maybe you’re in a post doc program, or have a nice job at Google or OpenAI with a steady salary, a clear trajectory, and instant street cred.

Do you still want to start a company?

Many first time founders start companies without realizing what it actually takes. Jensen Huang recently said he wouldn’t do it again.

Once you’ve started a company, you tend to be far more discerning before you go through it again – which is why second-time founders only go for it if they have an idea that’s really special.

(The risk for second time founders is “calling in rich” – i.e. when things get tough they wonder: why am I putting myself through this if I don’t have to?)

Part of the “charisma” of a successful startup founder comes from convincing investors you are strong enough to persevere through the suffering. So before you even consider pitching VCs, look at yourself in the mirror and be honest about whether you really want this.

If you understand all of this, convincing yourself you can and should start your company should be way harder than convincing investors. But if you are 100% bought in, your investors will know.

If you want this on a deep psychological level, it will show. Which leads to point #2….

Intangible #2: You Have To Do It

Most great founders start a company because they have to do it. Not necessarily because they want to do it. It’s a compulsion, rather than a choice.

There’s a reason the word “wantrapreneur” exists – it’s basically the polar opposite of this. It’s someone who wants to start a company because they perceive it to be glamorous.

This type of compulsion shows itself in the little actions and emotions you feel every day. You find yourself thinking about details of your startup in your “off” hours. Your browser history is filled with searches related to your company. Your friends and family will begin to find you annoying (see above re: suffering stoically). You’re so deep in the “idea maze” that you’re living in the future – it feels almost as real to you as the present.

I had a moment like that when I started my first company, Genome Compiler. I was working as a post doc at Stanford, right as it became clear that biology was becoming digitized. The idea of staying in academia, pipetting in the lab made me feel crazy. I had to be a part of enabling that techbio future, and I had the idea to help make it possible.

Then, a fellow post-doc from the lab next door actually left to start a company – it was the first time I realized that starting a company was something I could actually do. And I had to do it.

The best founders see the future as it could be. Eventually, you’ll become frustrated that the present is not as amazing as the vision of the future in your head. And in your mind, you will see a path – or several paths – to get there.

This is why I like to say that entrepreneurship is like a wormhole into a different reality. You have to follow that wormhole to that future you’ve created for yourself and everyone else.

If you need to do something that much, you’ll know. And so will your investors.

Intangible #3: You Authentically Care

Most founders are familiar with the idea of founder-market fit: the degree to which your expertise and skills align with the market you’re in. But I think there’s a level deeper than that: you don’t just know your market, you authentically care about it.

There are many people who are very good at a job that they simply don’t care about. It’s sad, but true. You can’t be one of those people if you want to start a company. You have to deeply care about the “why” behind what you’re doing. It’s easy to see in bio where we have examples of people trying to cure their families or friends.

If you care authentically, you’ll do the extra things that put you ahead of the competition. You’ll know the difference between meaningfully better and incremental. And, honestly, if you really care, you’ll find this fun.

This is actually your first step towards building a defensible company. If you care more than others, you’ll beat them.

Naval Ravikant has said it well: you escape competition through authenticity.

This is an area in which many people are unknowingly lying to themselves or to their VCs. Maybe you can convince yourself (and your investors) that you care about something for a few years. But you’ll never fake it throughout the 7-10 year relationship you have with a VC.

This kind of obsession doesn’t fade. You are okay with your company taking up 100% of your brain space because…it already is taking up that much space.

Don’t “fake it until you make it” – just be it.

Intangible #4: You Are “The Quarterback.”

The biggest part about being “compelling” to a VC is demonstrating that you can be a leader. We need to feel like we must invest in you. We want to be excited to introduce you to follow up investors, and feel proud to be associated with your company.

Again, this feeling is so subjective that it’s impossible to write a handbook. But I believe this intangible stems from a type of deep, multifaceted competence. You’re good with the big picture, and you’re also exceptional when it comes to the details.

You do the big things well. You can zoom out, look at your pitch and think strategically about raising money, making a business plan, sustaining the company as well as the product itself.

You do the small things well. If someone sends you an email, you answer quickly, with top level insight and just enough detail to be comprehensive, but not stuck in the weeds.

If you can do both of these things, you’re showing that you don’t just have the vision. You have the skills to execute.

That’s what a great quarterback does. They know where the ball should be, and have the talent to get it there –– even when there’s only a few seconds left to score.

Sell Yourself – Not Just Your Company.

If you are in the room for the right reasons, with the right team, and the right technology…you’ll be shocked at how easy it can be to raise money. But if you don’t realize how important YOU are in that story you’re going to struggle.

Many founders don’t realize that you’re selling yourself as much as you are your company during a pitch meeting.

If you are getting no after no – it might not be because of the idea. It might be how VCs are viewing you as the quarterback. This can be hard feedback to receive, which is why no one gives it. And not every VC is always right in this regard. Different VCs will have different takes on you. You won’t be for everyone and that’s fine. Just move on.

But if you can take a moment, and step back, this is just a new way to think about your pitch process.

Have the intangibles. Be the one. Then show us the intangibles. Show us you’re the one.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.