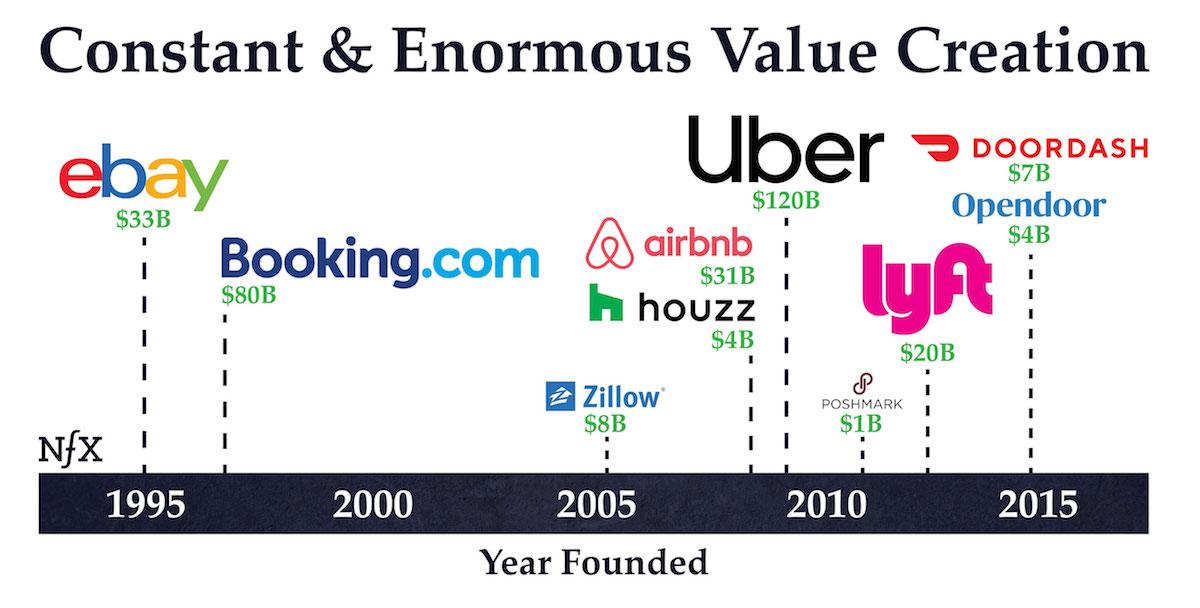

In 2019, two online marketplaces — Lyft, and Uber — will IPO for tens of billions of dollars.

With the level of success such companies have already seen, it’s easy for startup Founders to assume that all of the truly big opportunities have already been taken. In reality, nothing could be further from the case. The low-hanging fruit for online marketplaces may have been picked, but top Founders understand that the largest opportunities are often the hardest to grasp. The topmost branches of the tree can bear the richest rewards.

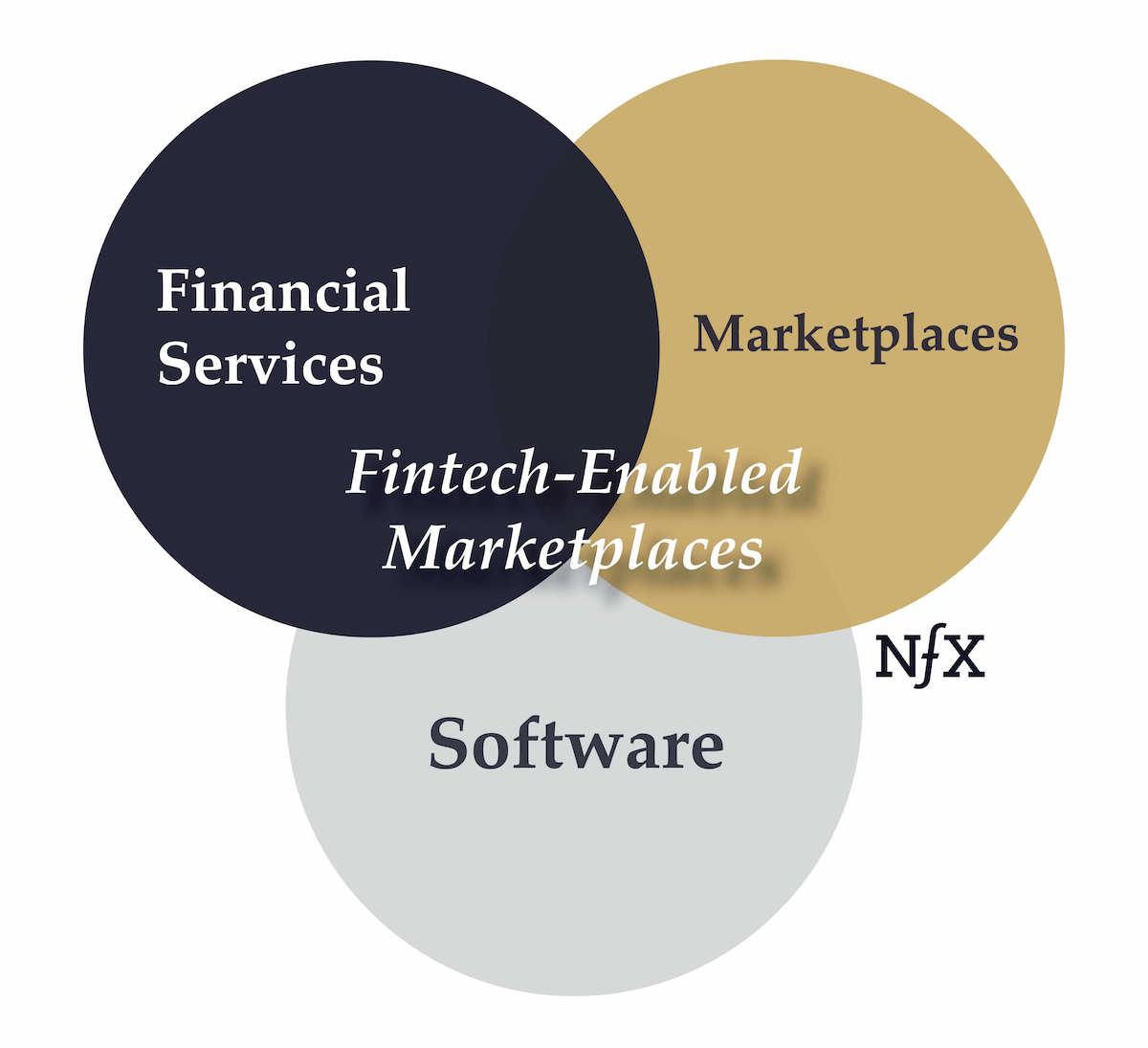

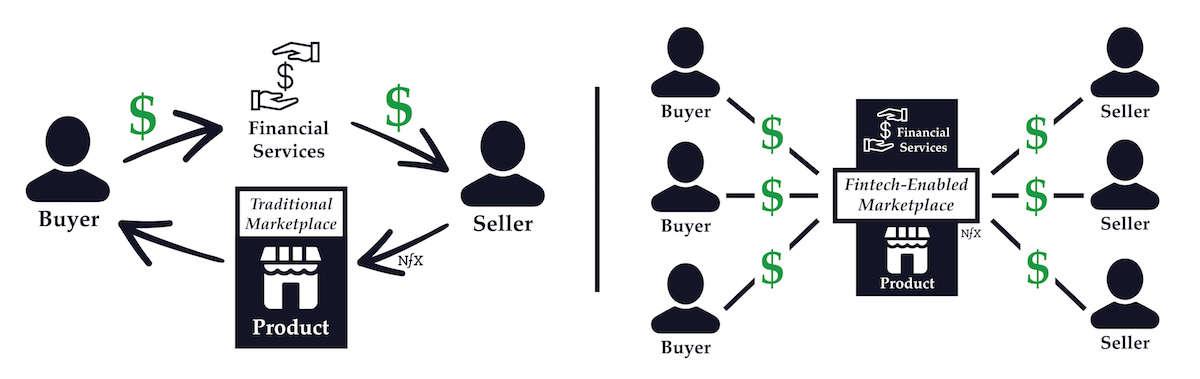

For 2-sided marketplaces, an extension to the traditional marketplace business model — incorporating financial services to enable new types of on-platform transactions — is the key to unlocking that higher level of opportunity. In this essay, we’ll explain why this apparently simple change will have enormous implications, and how it has already begun to define the next stage in marketplaces. We’ll also explain why what we’re calling fintech-enabled marketplaces have the potential to upend both traditional offline industries and incumbent marketplaces alike.

This last point is critical. As marketplaces encompass more of the transaction and tackle greater complexity in product offerings, we believe that they will bring laggard industries that have yet to be fully digitized, like education and healthcare, into the 21st century. In the process, whole new marketplace categories will be created. But what few realize is that the next generation of fintech-enabled marketplace startups will be a threat to incumbent online marketplaces as well. For Founders looking for opportunity where no one else sees it, understanding this is key.

The New Marketplace Playbook

To expand on what we introduced above, fintech-enabled marketplaces are marketplaces with tech-enabled financial services built directly into the platform. Recently, we’re seeing marketplaces begin to offer services like:

- Insurance: In-house insurance products made possible by better underwriting models

- Financing: Non-traditional financing options such as rent-to-own or income-sharing

- Banking: Novel and customer-specific solutions to manage transactions, deposits and payments.

AI and data advances are enabling all three of these buckets, because models for underwriting debt, insurance, and loans are becoming increasingly powerful thanks to AI and increased data exhaust. A number of B2B companies have also been popping up which leverage the growing amount of data available to be sourced or scraped from public sources and package it together to underwrite risk for their customers.

Leveraging new data sources and AI reduces the cost of underwriting via automation and improves loss ratios relative to more traditional underwriting or credit models. As a consequence, insurance and alternative financing options are becoming cheaper and more broadly applicable, expanding accessibility and giving rise to new use cases for debt and insurance that marketplaces can tailor to their specific needs.

Marketplaces containing one or more components that fall into the three buckets described above can be taken as a sign of the way things are headed. Some examples:

- Opendoor — leverages debt capital to provide instant liquidity for homesellers

- Lambda School — offers income-sharing for tuition financing as an alternative to student loans

- Fair.com — buys used vehicles and rents them out with a low-price month-to-month lease

- Airbnb — began offering a $1M insurance product not long after they launched, mitigating the risk of guests damaging their property for hosts

- Apple — in 2019, embedded financial services deeper into their iOS marketplace with the launch of Apple Card.

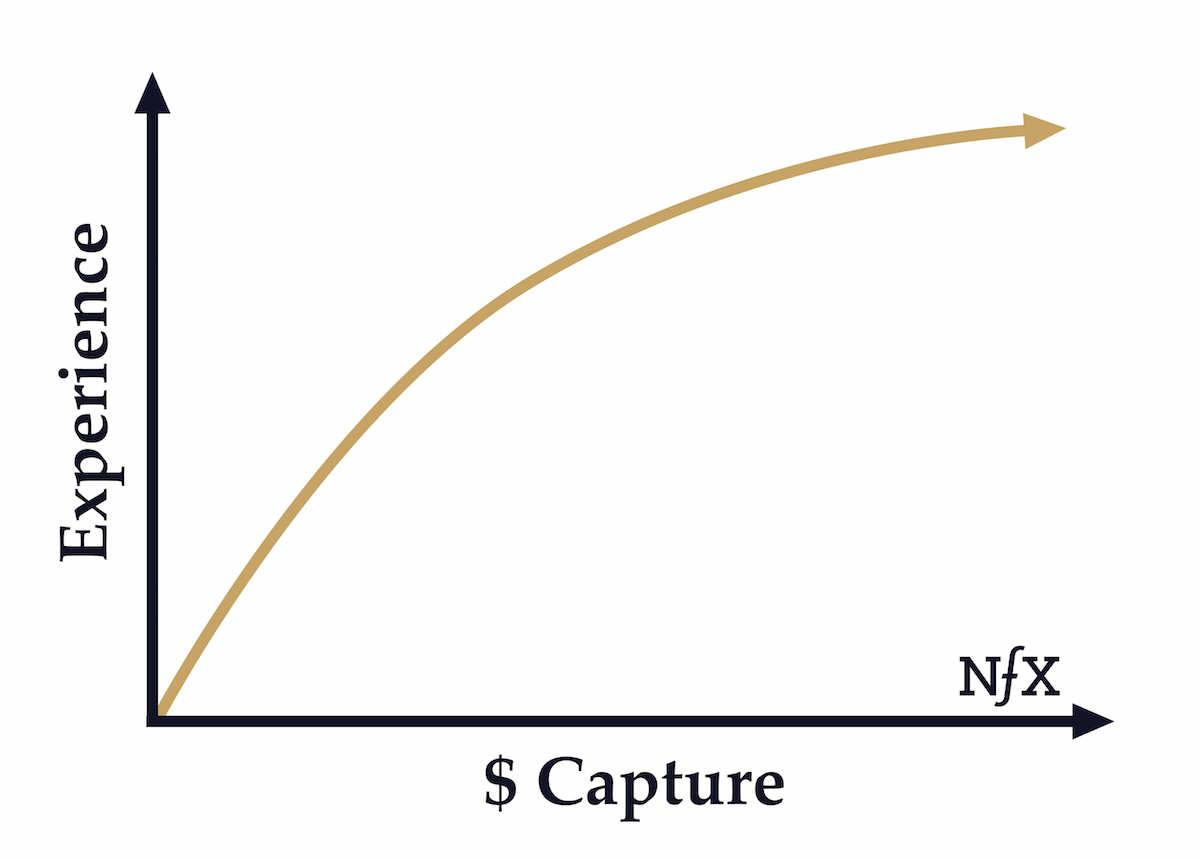

Incorporating fintech elements like this might seem like just an incremental change, but the effect can be revolutionary. By adding innovative financial services, marketplace startups can reduce the friction involved in (especially high-value) transactions for purchasers, and can improve incentive alignment amongst all parties with the removal of financial intermediaries between sellers and buyers. Importantly, this has the potential to lead to radical and breakthrough product experiences and let startups find a wedge into one or both sides of the market.

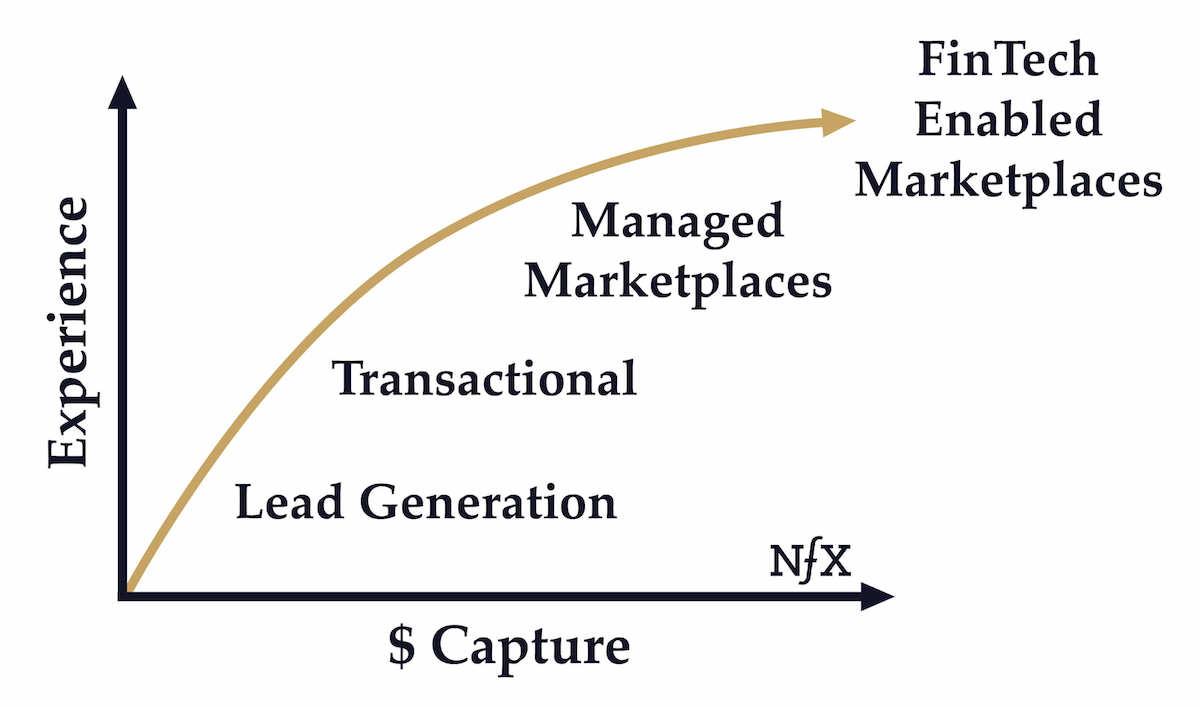

Based on broader trends in marketplace evolution, we can see that at each stage in the evolution of marketplaces, improved user experience has been a constant and unstoppable theme.

Patterns in Marketplace Evolution

Marketplaces have been highly effective in both unlocking and capturing economic value for two main reasons.

- Online marketplaces efficiently match the demand and supply sides in any given sector at massive scale

- 2-sided marketplaces are exceedingly defensible because when one side of the market gets “locked in”, the other can’t move — and vice versa. There has to be simultaneous movement of supply and demand to disrupt a marketplace once it has achieved critical mass.

The simplest online marketplaces, as in the early days of eBay or Craigslist, were listing services that own the discovery part of the funnel, putting buyers and sellers in touch but little more. Messaging, payment, user identity, user reputation, and everything else associated with the transaction takes place offline.

Since those early days, the trend has been towards marketplaces bringing more parts of the transaction on-platform. This, too, improves user experience by making transactions more seamless, while by capturing more of the transaction through scale or product innovation, marketplaces are able to charge higher take rates.

A side note: this evolutionary path applies specifically to 2-sided marketplaces. N-sided marketplaces, which require coordination of multiple supply-side parties to provide a complex service for a single buyer, branched off into a different evolutionary route we call market networks, which add layers of professional identity networking (e.g. LinkedIn) and SaaS workflow management to a multi-sided marketplace. For more on market networks, see our original essay.

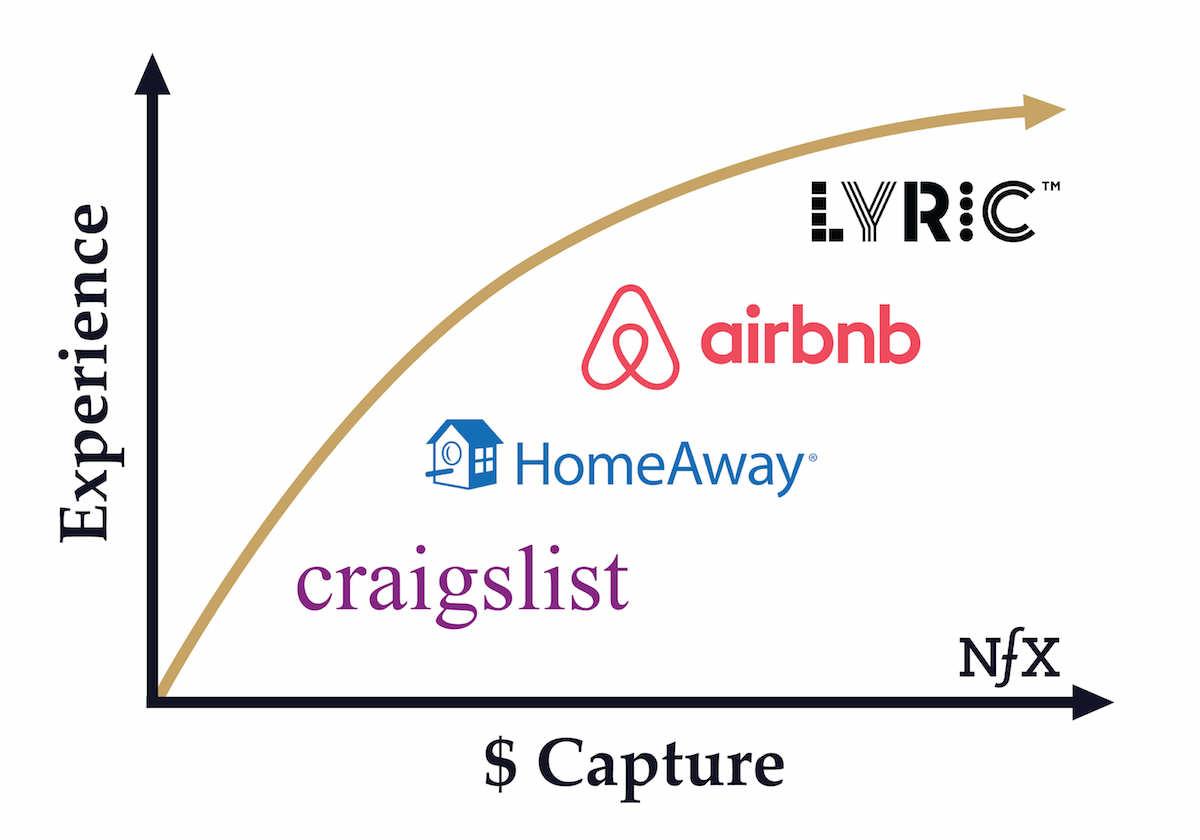

Returning to the evolution of 2-sided marketplaces, we have seen the trend illustrated above unfold across a number of market categories. For example, in hospitality, we see trends towards verticalization and toward bringing more of the listing, booking, and transaction processes online. We also see trends towards mobilization, tailoring an existing marketplace to a new platform and use-case, e.g. on-demand booking via HotelTonight. These changes have happened in roughly four phases.

- Horizontal lead generation — online discovery, offline booking e.g. Craigslist

- Vertical lead generation — verticalized discovery but offline booking e.g. HomeAway

- Vertical transactional — booking takes place entirely on-platform e.g. Airbnb

- Tightly managed marketplace — owning the whole supply experience, Lyric, Zeus, etc.

Each step of the evolution in hospitality marketplaces has so far brought more of the actual booking and transaction online, providing a more frictionless and catered user experience and increasing take rates.

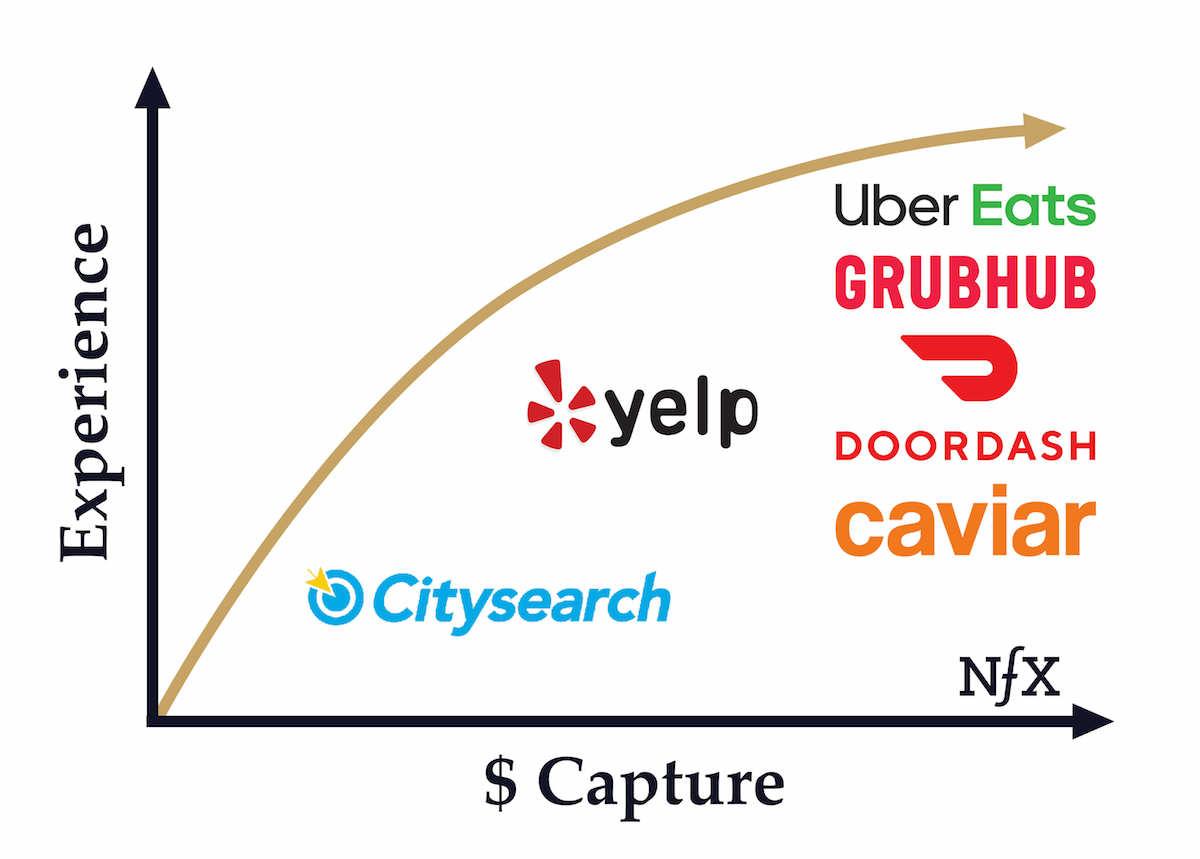

We see this same trend, from lead generation to owning the transaction, in food delivery, with on-demand delivery infrastructure serving as the equivalent of on-demand booking in the previous example.

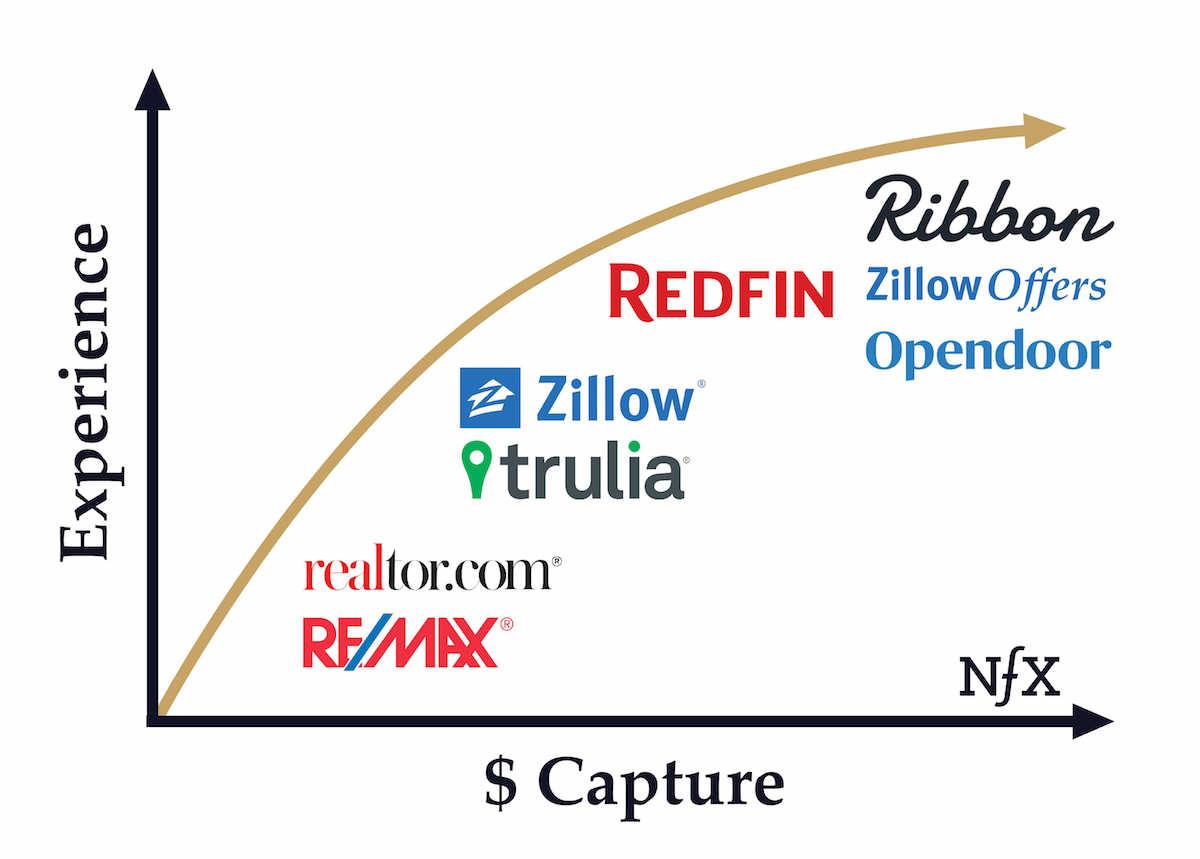

The same pattern appears yet again in real estate, which likewise went through four phases:

- Industry websites, e.g. Realtor.com

- Lead generation, e.g. Trulia and Zillow

- Managed transactional marketplaces, e.g. Redfin

- And finally, transactional marketplaces with major fintech components such as Opendoor, Ribbon and Zillow (more recently)

Across all these industries, a similar pattern appears if you look deeply: marketplaces bringing a bigger piece of the transaction online. Extrapolating to its logical extreme, this means bringing financial services online as well, since they’re necessary to intermediate transactions (especially big ticket items with high ASPs).

Why The Opportunity Is Now

In the past, we’ve written about why startup timing is everything. The evolutionary trends we’ve described only matter if the timing is right. There are four catalysts I’ve identified which make it the opportune time for Founders to work on fintech-enabled marketplaces:

- Consumer expectations are changing. Consumers have come to expect a seamless digital experience, and they crave immediacy — one-click transactions, frictionless on-platform, payment and financing, etc. Legacy brands have difficulty providing this.

- Money is already flowing through marketplaces. At this stage of evolution, customers have been habituated to spending money online. That trust can now extend further to other financial services.

- Better ML and data are improving underwriting. As mentioned earlier, the explosion in data exhaust, improvement in data collection techniques, and better ML algorithms capable of greater accuracy from smaller data sets allow new entrants to match or exceed underwriting capabilities of incumbents with years of data accretion.

- New fintech enabling technologies & capital. New enabling technologies have been developed around payments, banking, security, and identity which allow financial services to more easily be brought online and on-platform. Alongside this, the explosion of both debt and equity capital is a further catalyst for financial service offerings.

Punching Above Your Weight: 4 Advantages of Fintech-Enabled Marketplaces

The timing of Founders looking to start marketplaces incorporating fintech components is ripe, not only because of the catalysts mentioned above, but also because of the massive untapped opportunities presented by market inefficiencies stemming from misaligned incentives.

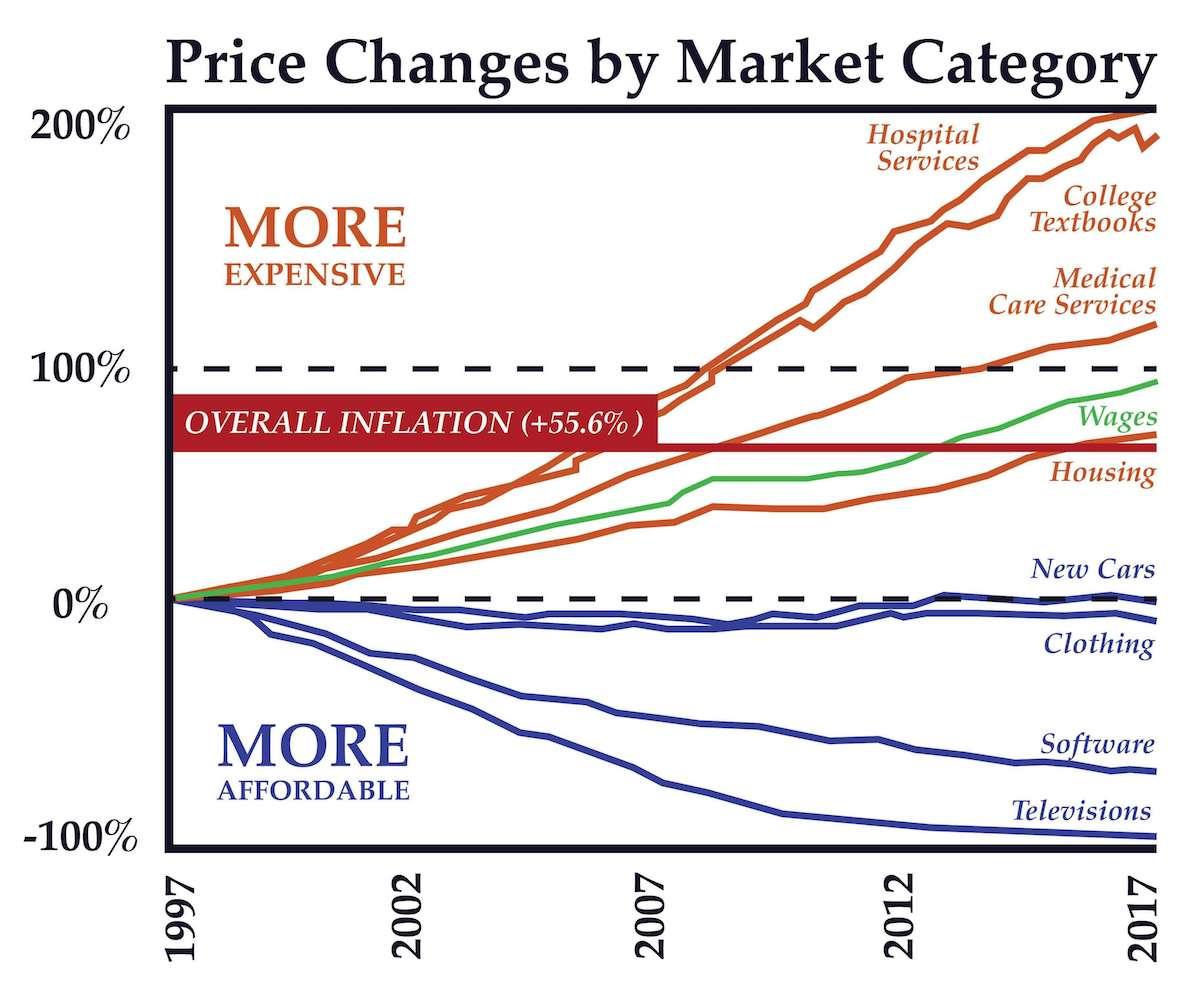

There’s an enormous white space for innovation and opportunity within major sectors which are plagued by misaligned incentives. You’ve probably seen the chart below, which shows price changes of US goods plotted against wages. In red are those industries which have seen prices increases that have outpaced wage inflation. In blue are those industries which have seen prices decrease relative to inflation.

The factor common to all the industries portrayed in red is that they’re often insulated from price competition due to misaligned incentives, often as a result of regulation or industry structure.

In medical services, for example, the incentives of the healthcare provider (supply side) are misaligned with that of the medical insurance provider, and those of the patient. The patient’s incentive is to maintain good health in the most cost efficient way.

Broadly speaking, the insurance provider’s incentive is to pay the least amount possible per patient relative to their insurance costs. And the medical provider is (financially) incentivized to bill insurance as much and as often as possible, regardless of what’s truly best for the health of the patient.

This misalignment partially explains the explosion of the cost of medical service with no attendant increase in its quality. The same applies for higher education, with heavily misaligned incentives between student loan companies, students, and universities.

As marketplaces continue their relentless push to capture more of the transaction and provide improved user experience, the path and opportunity for marketplaces to embed financial services is clear. For instance, high transaction value capture by financial services is one reason why 21% of Fortune 100 companies are financial services companies.

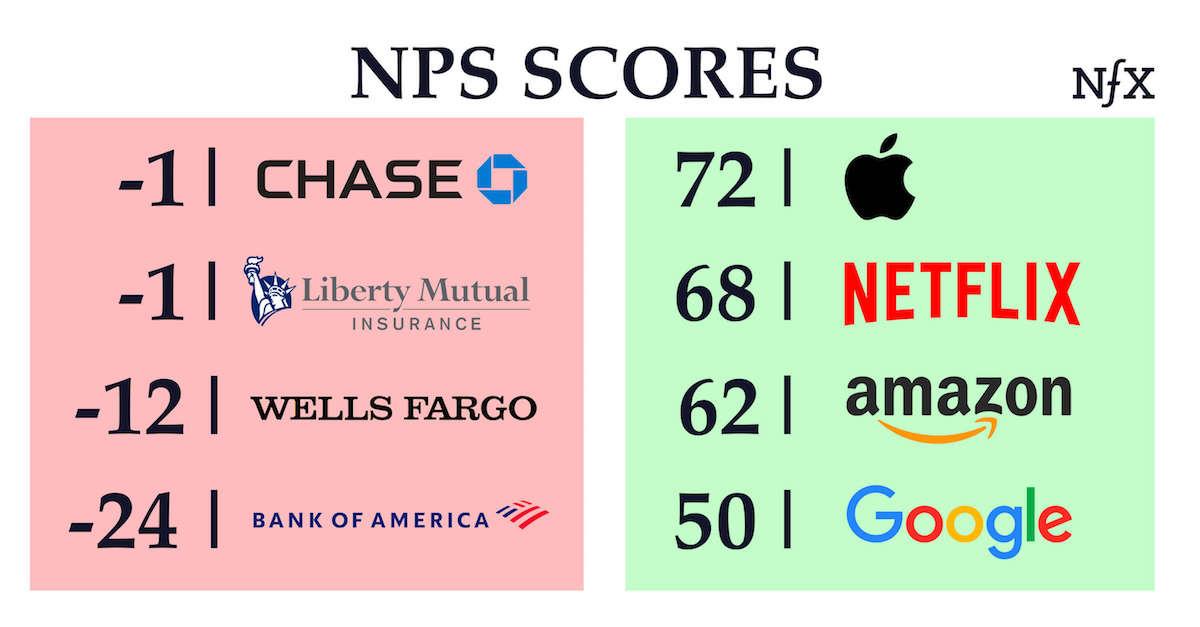

Yet, if you look at the NPS scores of financial services broadly, it’s clear that there’s a gap between their success and the value their providing. For example, here’s a comparison of the NPS scores of prominent financial service firms and a few top tech companies:

By integrating the third party and bringing financial services on-platform, fintech-enabled marketplaces will be well-poised to provide a superior user experience, allowing them to break into major industries with historically low tech penetration. On the flip side, by adding a marketplace network effect to financial services, fintech-enabled marketplace companies will enjoy a level of defensibility not traditionally seen in financial service companies.

Adding in financial service components, however, obviously comes with challenges because of the complexity involved. Leadership teams need to combine a strong capability to execute on product with a sophisticated understanding and execution ability of any financial services, legal or regulatory components. Incorporation of financial services, particularly with alternative financing products will often significantly increase the risk exposure of these businesses to economic cycles, and so they also need to thoughtfully construct a model that can navigate those cycles. While it can provide enormous leverage, the associated risk and complexity to the story and model can be off-putting to many investors.

Beyond eliminating misaligned incentives, fintech-enabled marketplaces will have other advantages over established marketplaces that will allow them to break into incumbent-dominated market categories. For example, they’ll be better positioned to:

1. Capture demand by removing friction

Fintech-enabled marketplaces can often build a breakthrough user experience to build liquidity and scale quickly.

Take Fair.com, an all-in-one long-term car rental company. It allows consumers to easily rent from their phone and swap cars whenever, removing a huge amount of transactional friction including buying, trading-in, insurance purchase, etc. Instead, it’s a simple purchase on your phone for a monthly fee.

Ribbon is another example which is backed by NFX. Ribbon gives the consumer freedom to buy their new home before they’ve sold their previous home, removing enormous friction from the complicated process of moving. The company has hundreds of millions of dollars of debt capital which acts as short-term bridge financing. Ribbon is paid a service fee to manage this process by the homeseller, which is often lower than the cash discount they’d typically pay.

2. Unlock latent supply

The smart use of capital, data, or insurance can be used to repurpose under-utilized assets. For example, offering $1M of insurance to hosts was the way that Airbnb got hosts to trust their homes to strangers. Careful readers of Lyft’s S-1 will likewise see that Lyft owns and operates its own insurance entity to cover drivers, a key risk-mitigation factor for the supply-side of a ridesharing marketplace. Marketplaces with enough debt capital can also unlock supply by using their balance sheet to acquire inventory themselves, e.g. OpenDoor buying itself to liquidity with real estate.

3. Reduce multi-tenanting by expanding buyer & seller relationships

Building incentives for both sides of the marketplace to stay in-network is a top priority for marketplaces. This is because multi-tenanting can drastically lower the defensibility of the business and allow competitors to gain ground. When there are low to non-existent switching costs, incentives to stay in-network are low, and marketplaces without such incentives not only run the risk of losing business to multi-tenanting but also to disintermediation, where the seller and buyer use the marketplace to find each other but then move their transactions offline to avoid the take rate.

By providing key financial services that enable the transaction, marketplaces can drastically improve the incentive for both sides of the market to keep their transactions both online and exclusive.

4. Subsidize product or marketing through bundling

Fintech-enabled marketplaces will have an advantage in that they’ll be able to capture more of the transaction value quickly by simultaneously selling more complementary goods or services to the same consumer. This can enable unprofitable marketing channels to become profitable by heightening ARPU at the same CAC, allowing for faster growth and enabling new paid marketing channels. Also, companies are bundling to pay for a better product experience, e.g. concierge services to improve user experience or renovation in the case of OpenDoor.

Platforms of the Future

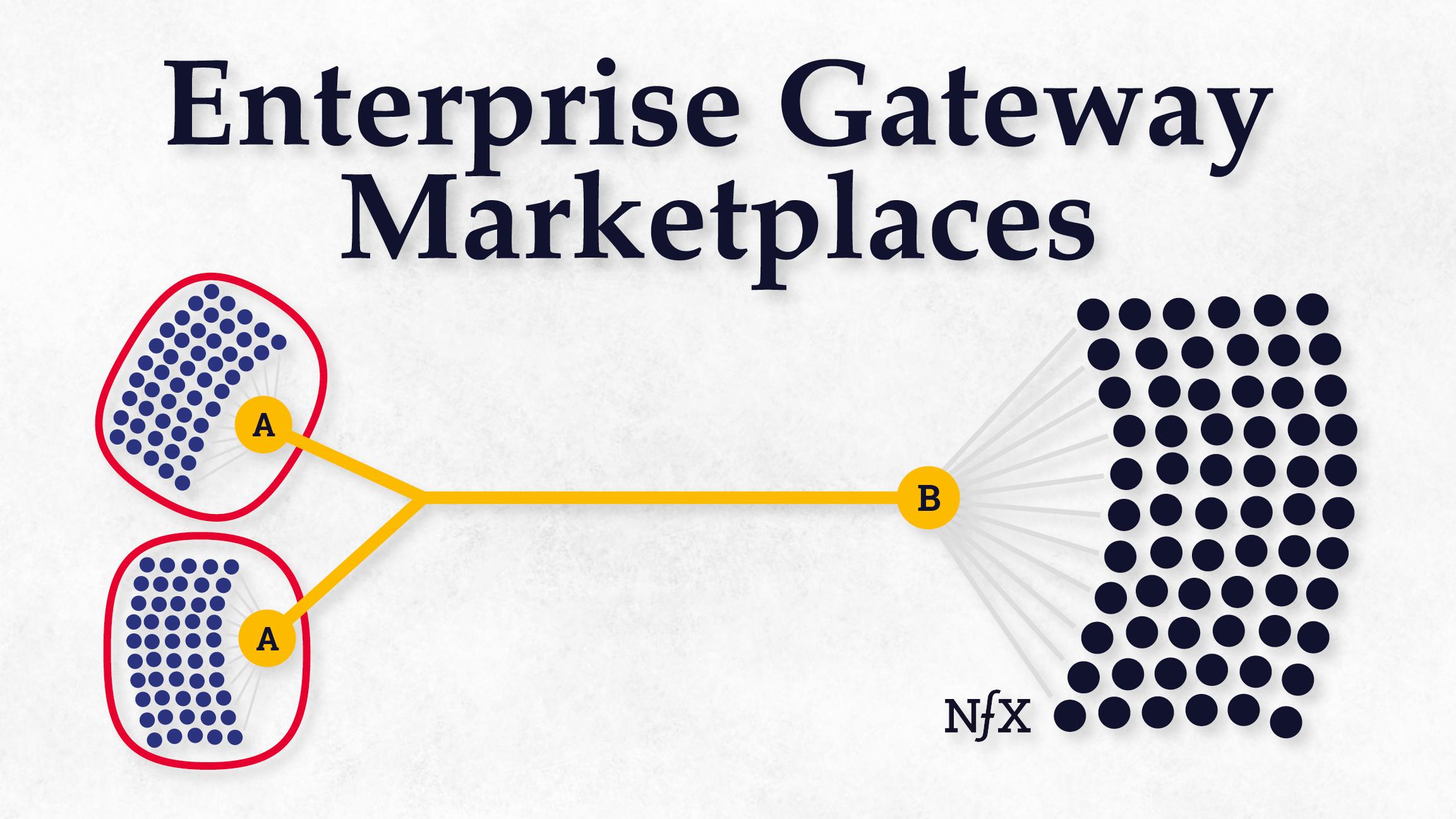

Before, we mentioned the fintech-enabling technologies that are powering the rise of fintech-enabled marketplaces. As more and more marketplaces incorporate this fintech component, companies with financial products that serve as a platform to enable fintech-enabled marketplaces will become increasingly common and lucrative. Early examples include:

For Founders, The Money Is In The Money

Ultimately, we see that for the next generation of marketplace startups, the money is in the money. This relentless drive towards a better experience and value capture will mean that the next set of billion dollar plus companies will be fintech-enabled marketplaces.

If you’re building a marketplace with fintech components like the ones we’ve described in this essay, or a platform to enable such marketplaces, we’d love to hear from you. Tell us about your company below and we’ll be in touch soon.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.