There’s only one thing you need to be an investor: capital. That’s it.

If all you do is raise money, have conviction, and invest in great companies, you’re ahead of 80% of investors in the game.

If you just invest in great companies and don’t create problems for your companies, you’re ahead of 90% of investors in the game.

And if you are the rare unicorn person who invests in great companies, adds positive value (beyond your capital) by being helpful to founders…that puts you in the top 1% of investors.

But it all comes down to raising capital. There are two ways to do that (other than being super rich). You can either join a fund with money or start one yourself.

Way more people should consider starting a fund. You can be what I call the “full stack VC.” The kind of investor that owns the whole process: raising money from LPs, sourcing and winning the best deals, supporting founders and helping lead the companies to exit (either IPO or M&A) to generate outsized returns.

If you do that, and become that 1% investor, you’ll have done something huge for everyone.

Step 1: Raise the Money

Maybe you have your own money from a big exit. In that case, congratulations, you can pay it forward for your industry and invest your own money right now. (Plus, your network and expertise will go a long way to helping you see, and win, better deals).

If you’re like most investors, you’re going to want to raise money from LPs (limited partners) anyway.

Again, anyone with a significant amount of capital can be an LP. But there are common sources most look to: university endowments, sovereign wealth funds, pension funds, foundations, funds of funds, family offices, etc. There’s no easy-to-find comprehensive list of LPs. But they’re findable if you’re enterprising about it. The real hard part is finding the right LP whose incentives align with yours.

Many LPs will have sweet spots the same way VCs do. A giant sovereign wealth fund won’t be interested in writing small $2M checks. A high net worth individual, though, might be perfectly happy to allocate a couple hundred thousand dollars to a new fund.

Interestingly, there are more LPs likely to take a chance on a first-time fund manager than you think. Data supports this decision. Since 1997, emerging managers have outperformed incumbents in terms of returns.

It makes sense. Young investors are infused with energy. They have a better understanding of new technologies, and are often more connected to other young founders. They think big.

If you’re good at raising as a freshman VC, it’s a good indicator you have a future. About 76% of first-time fund managers that raise more than $50m go on to raise a sophomore fund. But that will only happen if you are able to answer the three most important questions in this business:

Why you?

Why now?

How are you going to make outsize returns?

The Pitch

Before you even start creating the legal and financial infrastructure you need to become an investor, you have to answer the “why you” and “why now” questions.

The “why you”question is the most important part. There are many good answers to this question. You might have deep scientific expertise in a certain field, and know what would truly be revolutionary. You might have worked at a company with a “mafia” that’s a hotbed for future founders (like PayPal or SpaceX or Google). You might have deep connections within a specific industry network, and people are willing to send you deals.

My secret sauce was my experience as a scientist-founder. I was one of the first TechBio people who went through the entire cycle. I started going deep into research (Ph.D/Postdoc), founded my own company in the TechBio space very early on, suffered, learned and grew as a CEO, led a company through to a successful exit, joined a multi-billion leading company early on, and saw it scale first hand.

I know how it feels to live and breathe a techbio company, and (I hope) founders feel that way when they come to me.

Whatever your special sauce is, you need to convince your LPs that companies are going to come to you, and you are going to win those deals.

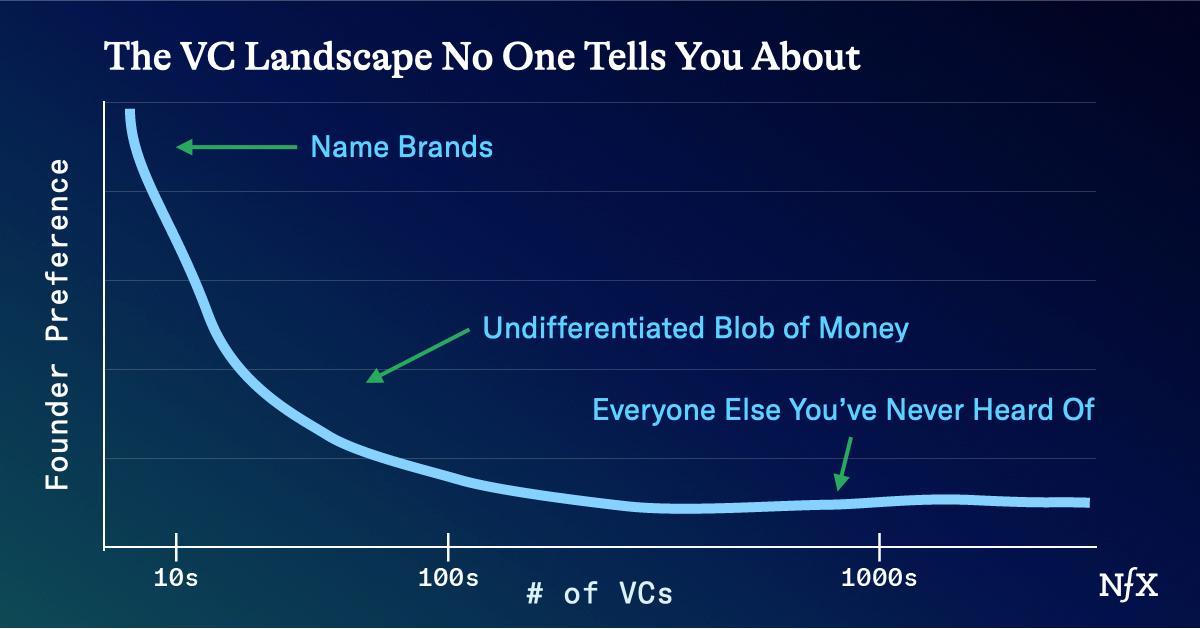

There are only a few funds who really do this well. I see the ecosystem this way:

There’s a few large, brand name funds. They don’t have to convince anyone that companies will come their way. Founders want to take their money because it makes them feel like they are the elite, smart chosen ones. Those brands make founders feel that everything will be easier: hiring, fundraising, PR, closing future deals.

Then, there’s the “undifferentiated blob of money.” These are the VCs founders find when they google “VC” and then spam all the relevant partners. Most founders will take your money, provided you’re not an asshole, but you’re not memorable or a first choice.

Finally, there’s the long tail. These VCs are happy to see a few deals, and when they see those deals, it’s probably because nobody else wanted them. These guys are like the suckers at the poker table – if you can’t spot who they are, there’s a chance it might be you.

The people that fall at the tall end of the power law are people that answered that “why you” question well, and built their success from there.

From there, you need to answer the “why now” question. You must have some conviction that now is a good time to invest in a certain space, using the skills unique to you.

For example, we often see founders who were early, successful entrepreneurs becoming investors because they see how much more growth there might be in a specific space. We even see successful entrepreneurs start funds investing in new areas that they find important for the world.

Riding a wave is a good enough “why now” reason to start a fund. But the “why you” question should outlive any potential trend. Trends come and go; your judgment is forever.

The most important thing is to keep your eye on the ball: The main thing LPs are judging is your chances of you generating outsized returns. But there are auxiliary reasons an LP might choose you over someone else. Some larger VCs might invest in smaller/earlier VC funds to help with deal sourcing and diligence, some corporate entities might invest in funds to learn about new trends and technologies, some sovereign wealth funds will invest for geo-political reasons. If you identify these strategies, tailor your pitch accordingly.

Set Your Fund Strategy

Next you have to decide the details of fund strategy. You can start with a few basic questions:

- How many checks are we going to write? Will you make a few concentrated investments or “spray and pray?”

- Are we going after any specific types of founders, or stages of company?

- How much money will we put aside for follow-up investments (this can be far more important than people think: a followup investment shows you still have conviction in a company – the lack of a follow up sends a telling signal).

- Other than money, what services will I offer founders?

- How will we define our fee structure? 2/20 (2% management fee and 20% carry), is the usual structure, but there are variations. It can be hard to survive and pay fund expenses on just 2% of a small fund. It’s possible to front-load the management fees in the early years to get on your feet.

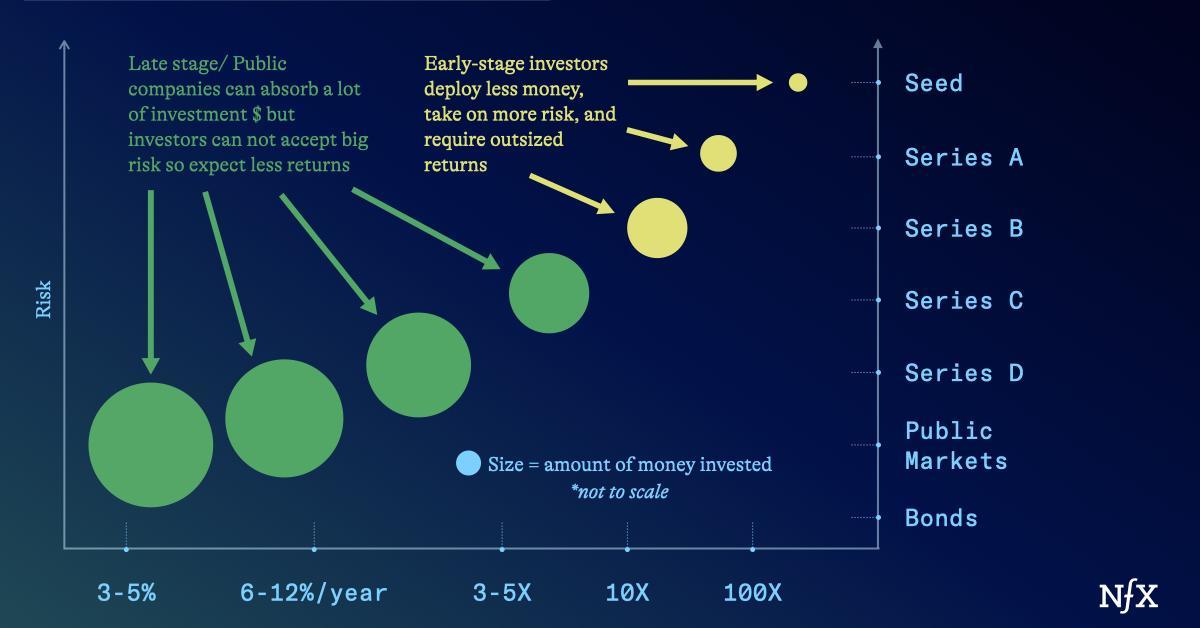

The size of your fund almost always dictates your strategy. For example, very small funds will struggle to compete at the later stages, so you may want to target early stage companies.

You always want the biggest return possible, no matter what fund size you are. But remember, the more you raise, the more money you need to return, and it becomes harder to make outsized returns

Sourcing and Winning

Sourcing is a major activity for most funds. You need to be able to see most of the qualified companies in your space to be able to pick the best ones – you can’t invest in a company you didn’t have a chance to meet!

You can focus on sourcing in many ways. Maybe companies come to you because of your past experience in an industry, maybe it’s a large social media following, or your thought leadership. Or you can build the right network through just plain hard work.

But if you have a good sourcing strategy, and have answered the “why you” question right, you will be seeing some deals. In fact, you should be generating enough inbound where your major problem is wading through it all.

The real challenge isn’t actually in sourcing lots of mediocre deals. It’s in winning the best deals.

There will only be a handful of great ideas and excellent teams each year that can create big enough companies to return a fund. Everyone will compete for them. The entire Silicon Valley ecosystem is built around this fiercely competitive dynamic.

If you’ve got what it takes, this should excite you. You must have conviction that you’re going to win those deals…or why even bother?

You can get a sense of whether you’re in line to win those big deals by how much you have to pay for them.

If you need to overpay for deals, that’s a bit of an indictment on you. They don’t see much non-financial value-add from your fund – but hey, at least you won the deal!

If you need to pay the same as someone else for deals, and founders still choose you, that’s a better sign. It’s a sign that you have preference compared to competitors.

The best sign is if you can pay less than your competitors. If you provide so much value that founders are willing to raise at a lower valuation, that’s a sign you’re doing something right. (Smart founders will always want to raise from the best investors at the right price.)

But you have to win and get allocation in the best deals – you can’t be an investor otherwise.

Judgment

Ground truth: most deals are bad, and great deals are rare.

It takes time to train your “investor neural network” on what great companies look like. Some great advice I got from a fellow investor was not to make any investment in the first 9 months. Almost every company looks worthy when you start investing. Over time investing gets harder and harder as you learn how rare amazing companies are.

If you know your stuff, these great deals will be obvious to you over time. In fact, the key skill won’t be identifying them…it’ll be winning them from other VCs. The best deals require the “offense mindset.”

Still, you need to learn how to find gems when you’re constantly “on defense.” That’s wading through the hundreds upon hundreds of companies you’ll hear from every day. In that pile, there will be some diamonds in the rough, some incredible IP, or a founder that maybe needs a nudge in a different direction.

Remember your only job is to invest in great companies. That means being ok not investing for long periods of time if you don’t find them or investing in several companies at the same time if they are all great.

Especially at the early stages, VC is still a data constrained field. The good news: there are a handful of companies that could be unicorns that are overlooked because humans forget, or make bad choices, or become assholes and leave those founders hanging. If you can see what others don’t you’ll go very far. (Pro tip: moving fast is a superpower).

At a very basic level, you need to learn to stay away from fraud. You know the type – companies that defy the laws of physics, or have questionable numbers.

Even after all of that, you will make mistakes. That’s fine. Even the best investors expect most of your early stage companies to not work out.

Helping: Becoming That Top 1% Investor

Sadly, many investors add negative value, despite the capital they bring to the table. Your first directive as an investor should be to “first do no harm.”

Helping a company succeed, though, will put you in rarified air. This is extremely difficult, and you probably won’t know if you’re actually helping a company for many years.

If you want to help your companies, it should be a push, not pull dynamic. You’re not on the ground with the company every single day, so you will always have a limited picture of what’s going on. Qualify all your advice appropriately if you do give it. Your advice carries weight and you can create damage.

That said, there are some areas where investors can be helpful to founders:

- Create the right connections

- Source follow-up investments

- Understand large market trends

- Help founders avoid extremely stupid mistakes (everyone needs a gut check once in awhile),

- Help hire top talent

- Help founders with mental health and when times are hard

- Give much needed tough love or kick in the butt

As an investor you have limited agency within the company. But when you are helpful and you see a company succeed, it’s the best feeling in the world (other than the money).

The Reason to Start a Fund

In 2021, everyone wanted to become a VC, and it was easy to raise. It attracted the wrong crowd. We don’t want people to get into VC because they think it’s easy or cool or the pathway to a lifestyle.

Now, interest rates are higher, and fewer are trying. But there’s still capital there for people with the vision and expertise to go after it. And you should go after it. We need people to get into VC because they have a vision for the future that others don’t, and believe they can make the vision a reality.

If we have the same types of people looking for the same types of investments, we’re never going to get big, radical ideas off the ground.

If scientists hadn’t become investors, we probably wouldn’t have the techbio space we have today. If programmers hadn’t become investors, we probably wouldn’t have the tech ecosystem we have today. If people who believe in longevity don’t invest, we’ll never get over the wall. Even today, less than 3 percent of biotech funding goes toward longevity.

I became an investor at NFX because I wanted to be the investor I wished I had when I was a Tech Bio founder. You can do the same thing. Fund the company you believe will generate 100x returns for humanity.

Take this essay as a way to reduce your activation energy, and go do it.

As Founders ourselves, we respect your time. That’s why we built BriefLink, a new software tool that minimizes the upfront time of getting the VC meeting. Simply tell us about your company in 9 easy questions, and you’ll hear from us if it’s a fit.